How AI Improves SME Financial Risk Management

9 Mar 2026

SMEs use AI for real‑time monitoring, predictive analytics and automation to reduce cash‑flow problems, fraud and bad debts while improving forecasting.

AI is helping small and medium-sized enterprises (SMEs) manage financial risks more effectively. By using tools that provide real-time monitoring, predictive analytics, and automated processes, SMEs can reduce risks like cash-flow issues, fraud, and bad debts. These tools, which were once only available to large corporations, are now affordable and accessible for smaller businesses through cloud-based platforms.

Key Takeaways:

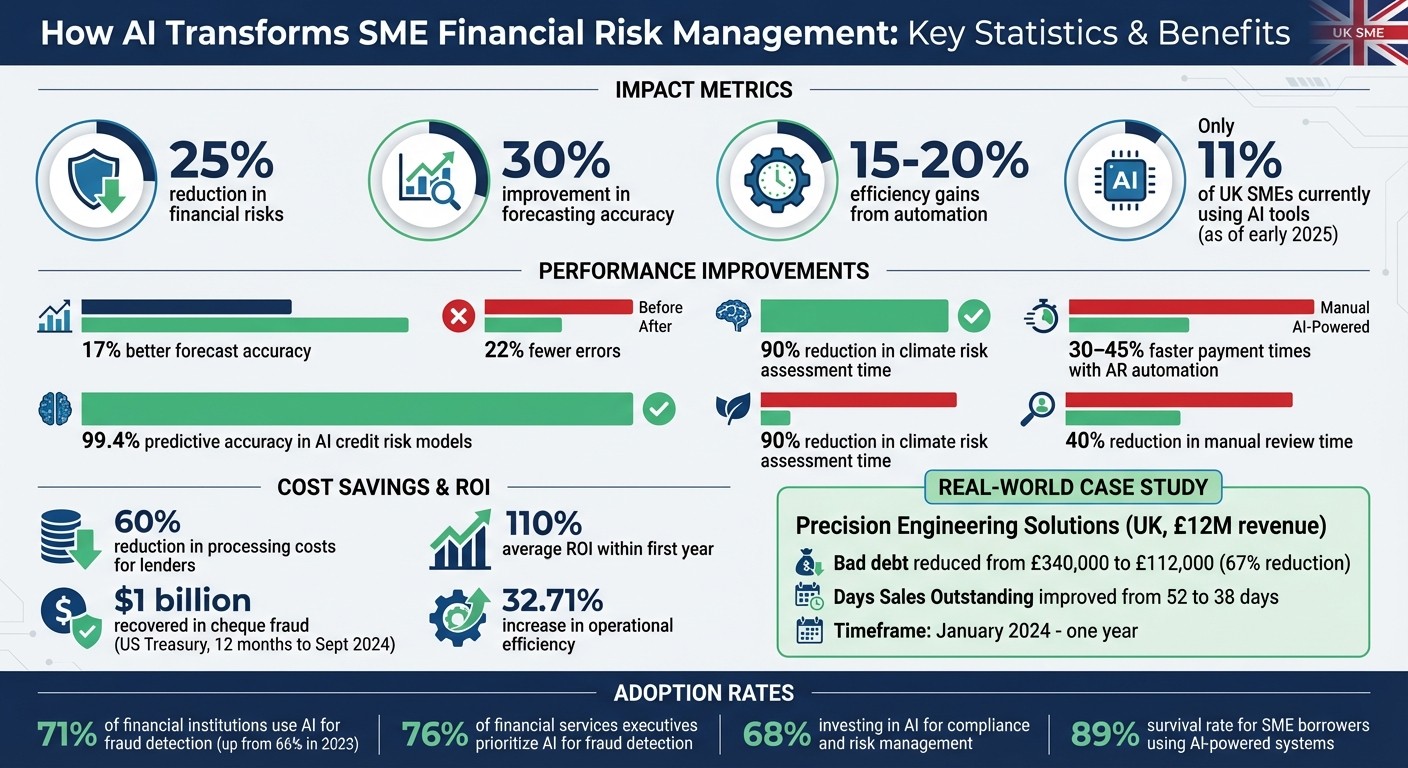

Risk Reduction: AI can lower financial risks by up to 25% and improve forecasting accuracy by 30%.

Real-Time Monitoring: Continuous tracking of financial data helps identify issues like late payments or fraud as they happen.

Predictive Analytics: AI forecasts risks and cash-flow problems weeks in advance, helping businesses plan better.

Automation: Automating tasks like invoicing and credit checks saves time and reduces errors, with efficiency gains of 15–20%.

Low Adoption Rates: As of early 2025, only 11% of UK SMEs were using AI tools, presenting an opportunity for businesses willing to invest.

SMEs that integrate AI into their financial processes can improve decision-making, protect their financial health, and gain a competitive edge. The article explores how AI identifies risks, offers solutions, and provides practical steps for implementation.

AI Financial Risk Management Impact: Key Statistics for SMEs

How AI Identifies Financial Risks Through Data Analysis

Traditional risk management often depends on static data snapshots - like monthly profit and loss statements, credit scores, or invoice deadlines. Meanwhile, AI takes a broader, more dynamic approach, analysing vast amounts of historical, market, and internal data continuously. This enables AI to spot warning signs that might slip past human analysts or standard spreadsheets.

Businesses using AI in financial risk management have reported 17% better forecast accuracy and 22% fewer errors. This improvement comes from AI's ability to detect complex, non-linear patterns - relationships between various risk factors that defy simple rules. For instance, deep learning can anticipate how delayed customer payments, rising supplier costs, and seasonal sales dips might combine to trigger a cash-flow crisis weeks before it happens. These capabilities form the foundation for the data-driven insights discussed next.

Using AI for Data-Driven Insights

AI goes beyond traditional financial checks. Instead of merely flagging overdue invoices, it analyses patterns in payment behaviour. It evaluates how quickly customers have paid in the past, whether payment times are growing longer, and what external factors might be affecting cash flow. This behavioural approach helps small and medium-sized enterprises (SMEs) anticipate cash-flow gaps well in advance.

Modern AI systems also pull in alternative data sources that traditional methods often overlook. These include social media sentiment, utility payment records, supply chain data, and customer reviews. Together, they provide a more complete assessment of risk. As Kiara Taylor from ACCA Global explains:

"The traditional approach often fails to capture the full picture of an SME's creditworthiness, leading to unfair assessments and missed opportunities".

Natural Language Processing (NLP) further enhances risk analysis by examining unstructured data, such as news articles, regulatory documents, and geopolitical updates.

AI-powered credit risk models are highly accurate, with some research use cases achieving predictive accuracy of 99.4%. Banks using generative AI have also drastically reduced the time needed for climate risk assessments by about 90%. For SMEs, these advancements shift the focus from reactive problem-solving to proactive planning, using scenario-based simulations to stress-test budgets against potential market changes.

Detecting Financial Irregularities

AI is particularly effective at spotting irregularities as they happen. Unlike manual audits, which are periodic and often uncover issues after the fact, AI provides continuous monitoring. It flags unusual transaction patterns in real time, identifying issues such as duplicate entries, irregular vendor payments, unrecognised transactions, overbilling, or unauthorised expenses by comparing current activity against historical behaviour.

For example, in the 12 months ending 30th September 2024, the U.S. Department of the Treasury used machine learning to recover $1 billion in cheque fraud. Closer to the UK, 71% of financial institutions now use AI for fraud detection, up from 66% in 2023.

Advanced AI systems also pick up on behavioural red flags that might indicate financial strain or fraud. These could include emotional distress in customer communications, inconsistent income declarations, or unusual payment routes. When irregularities are detected, AI generates instant alerts - often through visual dashboards that provide live updates on portfolio risk and liquidity status. High-priority cases are then escalated to professionals like accountants or underwriters for further review.

Risk Type | Traditional Identification Method | AI-Driven Identification Method |

|---|---|---|

Credit Risk | Credit scores and static financial statements | Real-time transaction patterns and alternative data |

Cash Flow Risk | Monthly P&L statements and invoice due dates | Behavioural analysis of historical payment timing |

Fraud Risk | Periodic manual audits and static rules | Real-time anomaly detection and pattern recognition |

Market Risk | Historical price spreadsheets | Real-time simulation of thousands of "what-if" scenarios |

Assessing Risks with AI Predictive Analytics

Once risks are identified using data-driven methods, the next step is assessing them. Unlike traditional forecasting, which often leans on historical averages, AI dives deeper, calculating probable risk scenarios with greater precision. This shift allows SMEs to transition from simply reacting to problems to planning ahead, understanding not just what might happen but also when and how it could impact their operations. Essentially, predictive analytics bridges the gap between spotting risks and turning those insights into actionable plans.

As Tipu Makandar puts it:

"Predictive analytics is not just fancy forecasting. It's an ecosystem of statistical models, machine learning, and real-time data analysis that builds probability scenarios."

AI-based tools, such as machine learning regressors and neural networks, often outperform traditional ratio-based methods in predicting financial outcomes and risks. Traditional approaches can be skewed by human biases - whether overly optimistic or overly cautious - while AI processes multiple variables simultaneously, offering a more balanced and accurate perspective.

Forecasting Financial Outcomes

AI predictive analytics draws from a mix of internal data, like sales figures, expenses, and cash flow, as well as external signals, such as market trends, economic indicators, and even weather patterns. This allows it to uncover complex relationships between risk factors. For example, AI might reveal how a 20% decline in sales, combined with rising raw material costs, could lead to a cash-flow crisis three months down the line.

Some tools offer SMEs a detailed 13-week cash flow forecast by analysing payment behaviours of both customers and suppliers. Platforms like Xero Analytics Plus, which projects future bank balances based on recurring bills and expected payment dates, and Pulse (aiPredict), known for advanced scenario planning, empower finance teams to run "what-if" simulations. These simulations stress-test budgets against potential market shifts.

AI can also uncover the true "Cost to Serve" by auditing client data. It identifies which customer segments are genuinely profitable and which consume excessive resources. This insight enables SMEs to allocate their resources more effectively and avoid overcommitting to accounts that don't deliver adequate returns.

While forecasts provide a forward-looking view, real-time scoring ensures risk assessments remain up to date.

Real-Time Risk Scoring

Traditional risk assessment often relies on static data - credit scores, invoice due dates, or monthly financial statements. AI, however, continuously evaluates real-time behaviours, such as payment patterns, rather than waiting for invoices to go overdue. These systems provide instant updates, recalculating risk scores as new transactions occur.

For instance, if a customer suddenly switches from BACS transfers to cheques or starts delaying payments by 10 days, AI flags these changes immediately. This allows SMEs to act quickly, preventing a minor issue from escalating into a serious cash-flow problem.

The rise of Explainable AI (XAI) has further enhanced these tools. Modern risk-scoring systems don’t just assign a score - they also explain the reasoning behind it, making decisions easier to justify to auditors and regulators.

Forecasting Approach | Traditional Method | AI Predictive Analytics |

|---|---|---|

Data Basis | Historical averages and static financial statements | Real-time transactions, market signals, and alternative data |

Update Frequency | Periodic (monthly or quarterly) | Continuous |

Insight Type | Reactive (what happened) | Proactive and predictive (what is likely to happen) |

Bias Risk | Human bias (overly optimistic or cautious) | Algorithmic bias if trained on flawed data |

Reducing Risks with AI Automation and Monitoring

AI’s ability to identify risks through data analysis is just the beginning. By combining automation with continuous monitoring, SMEs can now tackle risks in real time. Spotting potential issues is important, but the real advantage comes when AI not only flags these risks but also takes action to address them. Instead of relying on periodic reviews or audits, AI operates 24/7, triggering pre-set responses and highlighting problems as they occur. This shift from reactive to proactive management transforms how SMEs safeguard their financial health. It also paves the way for automated measures that further minimise risk.

Automated Risk Mitigation Strategies

With automated systems, actions can be taken instantly when a customer’s risk score drops below a certain threshold - no need to wait for human intervention. For instance, an SME could configure its AI to automatically adjust credit terms for customers scoring below 40 out of 100, while approving transactions immediately for those scoring 80 or above. This approach uses a weighted scoring system (e.g., 35% based on financial health, 30% on payment history), streamlining low-risk processes while ensuring high-risk accounts receive proper attention.

The benefits are striking. Businesses have reported efficiency gains of 15–20%, while lenders have seen processing costs drop by as much as 60%. These savings often come from automating time-consuming tasks like bookkeeping, invoicing, and bank reconciliation - tasks that previously relied on manual effort and were prone to errors.

Take Precision Engineering Solutions as an example. This UK-based manufacturing company, with £12 million in revenue, adopted a five-factor AI credit risk framework in January 2024. By scoring 180 customers and integrating early warning alerts, they slashed bad debt write-offs from £340,000 to £112,000 - a 67% reduction - in just one year. They also improved their Days Sales Outstanding (DSO) from 52 days to 38 days.

Continuous AI Monitoring for Risk Reduction

While automation handles immediate responses, continuous monitoring keeps an eye on emerging risks. Traditional methods rely on batch processes - monthly statements, quarterly reviews, or annual audits. AI, however, monitors financial transactions in real time, catching anomalies that might slip past manual checks.

Advanced systems go even further with dual-agent architectures. One agent engages with customers, while a secondary "silent" agent analyses communication patterns, such as tone, response delays, and inconsistencies. These subtle cues can flag risks like delayed statutory filings or key personnel changes. This approach has improved early risk detection by 30%.

AI doesn’t just notice issues - it acts instantly, often within milliseconds. For example, if a company delays statutory filings or experiences key personnel departures, AI flags these red flags immediately. This allows finance teams to step in before minor concerns grow into major cash flow problems.

Kristina Russo, CPA, MBA, and a representative of NetSuite, sums it up well:

"AI improves risk management by helping organisations identify, assess, control, and monitor financial risks with greater speed and accuracy than conventional methods can offer."

Beyond speed, these tools free up resources. AI-powered risk systems can cut manual review time by up to 40%, enabling finance teams to focus on strategic planning rather than routine checks. And the results are tangible: UK businesses using accounts receivable automation report 30% to 45% faster payment times, which directly boosts cash flow and reduces the ripple effects of late payments.

Using AgentimiseAI GuidanceAI for Tailored Risk Advisory

AI-driven automation can significantly reduce risks in real time, but its full potential is only realised when paired with strategic leadership. This approach transforms immediate insights into decisions that guide organisations proactively, ensuring businesses remain ahead of potential challenges.

While automated tools are effective, their true value emerges when combined with strategic leadership guidance. For many SMEs, accessing full-time CFOs or risk experts to interpret AI outputs and develop actionable strategies is often out of reach. This is where GuidanceAI steps in, acting as a virtual advisor that bridges leadership teams with specialised AI agents, supported by seasoned business professionals.

AI-Powered Leadership Advisory

GuidanceAI goes beyond data processing. It delivers context-specific recommendations tailored to the needs of UK SMEs, ensuring compliance with local regulations and practices. The platform begins by assessing a business’s readiness - evaluating factors like data infrastructure, adoption maturity, and team skill sets - before suggesting tools or strategies. This ensures that any AI-driven solution aligns with the company’s current operations, avoiding the pitfalls of generic, one-size-fits-all approaches.

One standout feature is the use of scenario modelling to explore financial outcomes. Leadership teams can simulate "what-if" situations, such as how a 15% improvement in forecasting accuracy might affect profit margins, before committing resources. By framing AI initiatives as testable hypotheses, GuidanceAI links technology directly to measurable financial results. It also identifies areas with the highest potential for risk reduction, presenting strong business cases with estimated savings and phased implementation plans.

This tailored guidance naturally evolves into customised automation, addressing the unique challenges SMEs face.

Custom AI Agents for SME Risk Management

GuidanceAI introduces custom AI agents designed to fit the specific workflows and processes of an SME. These agents handle routine leadership tasks - like performing process audits and identifying high-risk accounts - as the business grows. Unlike generic tools, these agents adapt to the particular challenges that consume resources, such as managing credit terms, monitoring cash flow, or overseeing supplier risks.

To roll out these tailored solutions, GuidanceAI recommends a phased approach: Foundation (assessing data and readiness), Implementation (testing with low-risk pilots), and Scale (expanding adoption across functions). This method mirrors successes seen in the financial sector, where institutions have reported 15% to 20% efficiency improvements after adopting AI-powered risk management. By combining AI’s precision and speed with human decision-making for critical tasks, SMEs gain the confidence to scale while staying in control.

How to Implement AI Risk Management: Step-by-Step Guide

Transitioning from planning to action requires a well-structured plan to integrate AI into financial risk management without disrupting daily operations. The following steps offer a practical framework that helps SMEs achieve progress through small, manageable successes rather than risky, large-scale changes.

Step 1: Map Current Financial Data and AI Tools

Before diving into technology, start by auditing your core financial processes. Identify 5–10 key workflows - like credit approvals, invoice handling, or supplier payments - and document their triggers, data flows, timelines, and common error points. This "process-first" approach ensures you avoid investing in tools that don't address your actual challenges.

Next, catalogue your data sources, including customer databases, financial records, supply chain logs, and even older spreadsheets. Pinpoint where your most reliable and centralised data resides - this is your "data gravity" and will form the foundation for any AI implementation. Check if your current platforms, such as Xero, QuickBooks, or your CRM, support open APIs for seamless integration. Also, ensure you have scalable cloud storage to handle AI's data demands.

Standardising naming conventions and consolidating platforms is crucial. AI relies heavily on clean, structured data, so investing time in data preparation is non-negotiable. To build a business case for AI tools, calculate ROI using this formula: (Current cost - Potential savings) / Implementation cost. Establish a steering committee with representatives from finance, IT, and leadership to align AI adoption with business objectives. Evaluate potential tools using the BXT Framework, which considers Business viability (ROI and strategy), Experience (user needs), and Technology (feasibility and risk). Then, categorise use cases into one of four groups: "Accelerate to MVP", "Incubate", "Research", or "Shelve."

Once your data is mapped and processes are audited, you can begin deploying AI in a controlled, low-risk setting.

Step 2: Deploy AI for Real-Time Risk Detection

Start small by launching low-risk pilots to build trust within your team. Instead of overhauling your entire system, leverage built-in AI features in tools you already use, like Xero, Shopify, or Salesforce. For quicker deployment, consider no-code AI platforms that allow you to roll out risk-monitoring tools in days, not months - minimising reliance on IT resources.

One effective method is dual-agent architecture: a "Main Agent" manages day-to-day tasks, while a background "Assistant Agent" monitors transactions for anomalies like tone changes, delays, or data inconsistencies. This setup enables real-time risk monitoring without disrupting existing workflows. For example, pilot programmes have shown reductions in bad debt and improvements in cash flow metrics.

If you’re testing with public AI models, anonymise sensitive transaction data by exporting it to CSV and stripping out customer details. Also, define clear escalation protocols so that AI can flag issues like financial strain, emotional distress, or legal concerns for human review.

Step 3: Validate AI Outputs with Human Oversight

AI should assist in identifying risks, not replace human judgement. Think of AI as a "Virtual CFO" that highlights potential issues while leaving critical decisions to your team. Set clear risk thresholds, such as requiring manual CFO approval for credit scores below 40 or transactions exceeding £25,000. This allows AI to handle routine tasks while experts focus on complex cases.

Invest in Explainable AI (XAI) tools that provide clear reasoning behind risk scores. Transparency is vital for audits, lender discussions, and building internal trust. Add fact-checking layers to cross-verify AI outputs with your internal data. Regularly review AI performance - monthly or quarterly - to compare predicted risk scores with actual outcomes. Adjust model weightings based on these insights and track metrics like "False Positives" (rejected good customers) and "False Negatives" (approved bad debt) to evaluate reliability. By reducing manual review time by up to 40%, AI tools free up your team to focus on more strategic decisions.

AI Tools Comparison Table

Choosing the right AI tool depends on your SME's specific financial risks. For instance, Predictive Analytics is ideal for forecasting cash flow gaps by analysing historical payment patterns rather than relying solely on invoice due dates. Meanwhile, Monte Carlo Simulations allow you to stress-test budgets through thousands of "what-if" scenarios. On the other hand, Value at Risk (VaR) Analysis quantifies the maximum potential financial loss over a set timeframe, simplifying complex data into easy-to-understand risk classes (e.g., A1–E3), which lenders and auditors can readily interpret.

Here's a table that breaks down the core differences between these AI tools, making it easier to determine which one aligns with your needs:

AI Tool | Primary Function | Integration Method | Ideal For |

|---|---|---|---|

Predictive Analytics | Forecasts future cash flow, revenue trends, and credit default probabilities | Integrates with cloud accounting platforms (e.g., Xero, QuickBooks) to analyse historical and market data | Managing cash flow volatility and liquidity gaps |

Monte Carlo Simulations | Tests business resilience by simulating thousands of "what-if" scenarios | AI engines generate multiple variations simultaneously to uncover hidden risk correlations | Strategic planning and mitigating market risks |

Value at Risk (VaR) | Quantifies maximum potential financial loss over a specific timeframe | Processes unstructured data and real-time market volatility to dynamically update loss estimates | Credit risk assessment and meeting regulatory compliance |

This table complements earlier discussions, offering a streamlined way for SMEs to align their risk management strategies with the right AI tools. Notably, in SME credit rating models, payment behaviour accounts for 24% of the weighting, followed by corporate profitability at 19% and debt ratios at 15%. This highlights the critical role of tools that monitor payment patterns in shaping risk profiles. By leveraging affordable, cloud-based platforms, SMEs can access enterprise-level capabilities without the need for an in-house data science team.

Measuring AI Impact on Financial Risk Reduction

Key Performance Indicators for AI-Driven Risk Management

To ensure AI investments deliver tangible financial results, it's crucial to measure performance using the right metrics. Start with financial impact metrics like ROI, calculated as (Net Benefits / Total Costs) × 100. Benefits often include savings on labour, reduced error costs, and fraud prevention. For instance, a UK-based SME achieved an impressive ROI by automating routine financial tasks, saving £10,000 in labour costs while generating £50,000 in new revenue through better targeting and forecasting. On average, AI projects deliver at least 110% ROI within the first year.

In addition to ROI, track risk-specific KPIs that highlight how AI helps protect financial assets. Metrics like reduced fraud-related losses, improved cash flow stability through predictive forecasting, and quicker risk resolution - such as cutting loan approval times from weeks to minutes - are key. Operational efficiency can also be measured with the automation ratio (the percentage of tasks like underwriting or bookkeeping handled by AI) and the time saved per financial process. To ensure AI remains effective, monitor technical metrics like the F1-score (which balances precision and recall in fraud detection) and model drift (a decline in accuracy over time).

Before deploying AI, establish a baseline by measuring how long and costly manual processes currently are. For example, if summarising a report takes 25 minutes manually, this benchmark will help quantify the time saved by automation. This step ensures you're comparing actual performance gains rather than relying on inflated expectations. As highlighted in the IBM 2025 CEO Study:

"65% of CEOs prioritise AI initiatives based on ROI, but only 52% say their generative AI investments provide value beyond cost savings".

These metrics not only provide immediate insights into AI’s effectiveness but also lay the groundwork for building long-term financial stability.

Long-Term Benefits of AI Adoption

The advantages of AI extend far beyond short-term cost reductions. SMEs, for example, have increased operational efficiency by over 32.71% through AI adoption. Moreover, continuous AI monitoring significantly boosts survival rates for SMEs. Studies show that AI-powered financial systems contribute to an 89% survival rate for SME borrowers, alongside consistent revenue growth.

AI's ability to democratise advanced risk management tools is particularly transformative. Features once limited to major financial institutions are now accessible to SMEs through affordable cloud-based platforms. This not only levels the playing field but also helps businesses build resilience against market fluctuations. Regular reviews - such as quarterly assessments - can help identify new AI features, refine workflows, and determine whether deeper integrations are needed. By combining AI with human oversight, businesses can surface risks effectively while reserving critical decisions for human judgement. Treating AI as a collaborative "assistant" rather than a standalone solution turns it into a driver of sustained growth and competitive strength.

This balanced approach ensures AI delivers more than just one-off efficiency gains, laying a foundation for long-term financial health and resilience. With the right metrics and strategies in place, AI-driven risk management can become a cornerstone of SME success.

Conclusion

AI is reshaping how SMEs approach financial risk management, shifting the focus from reactive responses to proactive, data-driven strategies. With tools that offer 24/7 monitoring, real-time anomaly detection, and predictive analytics, businesses can spot risks before they materialise. This shift has been shown to reduce financial risk by up to 25% and improve forecasting accuracy by 30%. What’s more, these advanced tools - once exclusive to large financial institutions - are now accessible to founder-led businesses via affordable, cloud-based platforms.

By automating repetitive tasks like invoice processing and reconciliation, AI can cut manual review time by as much as 40%. This frees up finance teams to concentrate on strategic decision-making. As Dieu Anh Nguyen of Verysell AI explains:

"AI frees accounting teams from manual tasks and lets finance become a 'value-creator'".

This efficiency doesn’t just save time - it also saves money. Lenders have reported up to 60% reductions in processing costs, while dual-agent systems enhance early risk detection by 30%.

For SMEs looking to implement AI, platforms like AgentimiseAI and GuidanceAI provide tailored solutions. These tools act as virtual C-suite advisors, offering high-level risk management insights without the need for costly full-time executives. Designed specifically for founder-led SMEs, they combine continuous monitoring with expert guidance, delivering boardroom-level advice at a fraction of the cost.

The growing adoption of AI is clear: 76% of financial services executives now prioritise AI for fraud detection, and 68% are investing in AI for compliance and risk management. For SMEs, starting with simple automations and ensuring high-quality data lays a strong foundation. Crucially, maintaining human oversight for critical decisions ensures AI complements, rather than replaces, human judgement. By treating AI as a collaborative partner, SMEs can confidently use it to strengthen their financial stability.

FAQs

What data do I need before using AI for financial risk management?

To leverage AI in financial risk management effectively, you'll need several key data types:

Accurate financial data, such as cash flow, budgets, and financial statements, to generate dependable insights.

Historical data, including customer payment records, credit histories, and market trends, to spot patterns and anticipate potential risks.

Compliance data, like VAT details and UK regulations, to ensure all activities align with legal requirements.

Customer and supplier data, covering creditworthiness and payment histories, to evaluate credit risks effectively.

Real-time transaction data, which supports dynamic forecasting and allows for proactive risk management.

These data sources form the backbone of AI-driven financial risk strategies.

How can I pilot AI risk tools without disrupting daily finance work?

Start with small, low-risk projects that address specific challenges, such as cash flow forecasting or compliance monitoring. Make sure your data is well-organised and accurate, and bring your finance team on board early to ensure the integration process runs smoothly. Opt for no-code or rapid deployment AI platforms to implement solutions quickly and efficiently. Track the performance of these tools, adjust them based on feedback, and once they demonstrate success, gradually introduce them to other areas of your finance operations.

How do I keep AI risk scores accurate and explainable over time?

To keep AI risk scores accurate and clear, it’s crucial to routinely review outputs, ensure clarity in how scores are calculated, and update models with fresh data. Regular monitoring and validation play a key role in identifying and addressing any weak points. Tools such as GuidanceAI by AgentimiseAI provide a helpful solution, linking leadership teams with AI agents trained by human experts. This ensures expert advice and oversight are available to support dependable decision-making.